Rolling Regression

Rolling regressions are one of the simplest models for analysing changing relationships among variables overtime. They use linear regression but allow the data set used to change over time. In most linear regression models, parameters are assumed to be time-invariant and thus should not change overtime. Rolling regressions estimate model parameters using a fixed window of time over the entire data set. A larger sample size, or window, used will result in fewer parameter estimates but use more observations. For more information, see Base on Rolling.

Keep in Mind

- When setting the width of your rolling regression you are also creating the starting position of your analysis given that it needs the a window sized amount of data begin.

Also Consider

- An expanding window can be used where instead of a constantly changing fixed window, the regression starts with a predetermined time and then continually adds in other observations until the entire data set is used.

Implementation

Python

This example will make use of the statsmodels package, and some of the description of rolling regression has benefitted from the documentation of that package.

Rolling ordinary least squares applies OLS (ordinary least squares)

across a fixed window of observations and then rolls (moves or slides)

that window across the data set. The key parameter is window, which

determines the number of observations used in each OLS regression.

First, let’s import the packages we’ll be using. If you don’t already

have these installed, open up your terminal (aka command line) and use

the command pip install packagename where ‘packagename’ is the package

you want to install.

from statsmodels.regression.rolling import RollingOLS

import statsmodels.api as sm

from sklearn.datasets import make_regression

import matplotlib.pyplot as plt

import pandas as pd

Next we’ll create some random numbers to do our regression on

X, y = make_regression(n_samples=200, n_features=2, random_state=0, noise=4.0,

bias=0)

df = pd.DataFrame(X).rename(columns={0: 'feature0', 1: 'feature1'})

df['target'] = y

df.head()

| feature0 | feature1 | target | |

|---|---|---|---|

| 0 | -0.955945 | -0.345982 | -36.740556 |

| 1 | -1.225436 | 0.844363 | 7.190031 |

| 2 | -0.692050 | 1.536377 | 44.389018 |

| 3 | 0.010500 | 1.785870 | 57.019515 |

| 4 | -0.895467 | 0.386902 | -16.088554 |

Now let’s fit the model using a formula and a window of 25 steps.

roll_reg = RollingOLS.from_formula('target ~ feature0 + feature1 -1', window=25, data=df)

model = roll_reg.fit()

Note that -1 just suppresses the intercept. We can see the parameters

using model.params. Here are the params for time steps 20 to 30:

model.params[20:30]

| feature0 | feature1 | |

|---|---|---|

| 20 | NaN | NaN |

| 21 | NaN | NaN |

| 22 | NaN | NaN |

| 23 | NaN | NaN |

| 24 | 20.736214 | 35.287604 |

| 25 | 20.351719 | 35.173493 |

| 26 | 20.368027 | 35.095621 |

| 27 | 20.532655 | 34.919468 |

| 28 | 20.470171 | 35.365235 |

| 29 | 20.002261 | 35.666997 |

Note that there aren’t parameters for entries between 0 and 23 because our window is 25 steps wide. We can easily look at how any of the coefficients are changing over time. Here’s an example for ‘feature0’.

fig = model.plot_recursive_coefficient(variables=['feature0'])

plt.xlabel('Time step')

plt.ylabel('Coefficient value')

plt.show()

Recursive ordinary least squares (aka expanding window rolling regression)

A rolling regression with an expanding (rather than moving) window

is effectively a recursive least squares model. We can perform this kind

of estimation using the RecursiveLS function from statsmodels.

Let’s fit this to the whole dataset:

reg_rls = sm.RecursiveLS.from_formula(

'target ~ feature0 + feature1 -1', df)

model_rls = reg_rls.fit()

print(model_rls.summary())

Statespace Model Results

==============================================================================

Dep. Variable: target No. Observations: 200

Model: RecursiveLS Log Likelihood -570.923

Date: Sun, 23 May 2021 R-squared: 0.988

Time: 17:05:03 AIC 1145.847

Sample: 0 BIC 1152.444

- 200 HQIC 1148.516

Covariance Type: nonrobust Scale 17.413

==============================================================================

coef std err z P>|z| [0.025 0.975]

------------------------------------------------------------------------------

feature0 20.6872 0.296 69.927 0.000 20.107 21.267

feature1 34.0655 0.302 112.870 0.000 33.474 34.657

===================================================================================

Ljung-Box (Q): 40.19 Jarque-Bera (JB): 3.93

Prob(Q): 0.46 Prob(JB): 0.14

Heteroskedasticity (H): 1.17 Skew: -0.31

Prob(H) (two-sided): 0.51 Kurtosis: 3.31

===================================================================================

Warnings:

[1] Parameters and covariance matrix estimates are RLS estimates conditional on the entire sample.

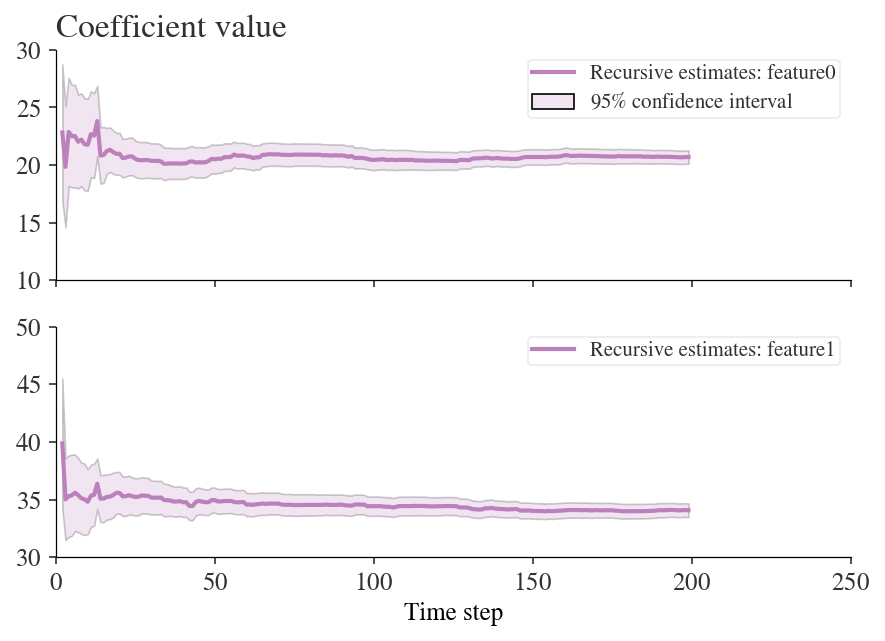

But now we can look back at how the values of the coefficients changed in real time:

fig = model_rls.plot_recursive_coefficient(range(reg_rls.k_exog), legend_loc='upper right')

ax_list = fig.axes

for ax in ax_list:

ax.set_xlim(0, None)

ax_list[-1].set_xlabel('Time step')

ax_list[0].set_title('Coefficient value');

R

In R the rollRegres (one s, not two) package can compute rolling regressions while being able to specify the linear regression, window size, whether you want a rolling or expanding window, the minimum number of observations required in a window, and other options.

#Load in the package

library(rollRegres)

The data will be manually created where x can be interpreted as any independent variable over a fixed time period, and y is an outcome variable.

#Simulate data

set.seed(29132867)

n <- 200

p <- 2

X <- cbind(1, matrix(rnorm(p * n), ncol = p))

y <- drop(X %*% c(1, -1, 1)) + rnorm(n)

df_1 <- data.frame(y, X[, -1])

#Run the rolling regression (Rolling window)

roll_rolling <- roll_regres(y ~ X1, df_1, width = 25L, do_downdates = TRUE)

#Check the first 10 coefficients

roll_rolling$coefs %>% tail(25)

## (Intercept) X1

## 176 1.467609 -1.1887381

## 177 1.561271 -1.0356878

## 178 1.598559 -1.0142755

## 179 1.615713 -0.8161185

## 180 1.680253 -0.8814448

## 181 1.593962 -0.8878947

## 182 1.623287 -1.0246186

## 183 1.596735 -1.0535530

## 184 1.761971 -0.9466231

## 185 1.703679 -0.8138562

## 186 1.619849 -0.8948204

## 187 1.729696 -0.9266218

## 188 1.606376 -1.0624713

## 189 1.676579 -0.9823355

## 190 1.657288 -1.0377997

## 191 1.579115 -1.1432474

## 192 1.586334 -1.1829136

## 193 1.393517 -1.1447650

## 194 1.250160 -1.0244144

## 195 1.243020 -1.0232251

## 196 1.205068 -1.0201693

## 197 1.273287 -0.9792404

## 198 1.336927 -0.9346933

## 199 1.343452 -0.9316855

## 200 1.284072 -0.9379035

To demonstrate the point about a starting position for your analysis, the entries up to 24 are null because of the choice of window size.

#Check the first 25 coefficients

roll_rolling$coefs %>% head(25)

## (Intercept) X1

## 1 NA NA

## 2 NA NA

## 3 NA NA

## 4 NA NA

## 5 NA NA

## 6 NA NA

## 7 NA NA

## 8 NA NA

## 9 NA NA

## 10 NA NA

## 11 NA NA

## 12 NA NA

## 13 NA NA

## 14 NA NA

## 15 NA NA

## 16 NA NA

## 17 NA NA

## 18 NA NA

## 19 NA NA

## 20 NA NA

## 21 NA NA

## 22 NA NA

## 23 NA NA

## 24 NA NA

## 25 1.401621 -1.127908

Finally, here are the results when using an expanding window (also known as recursive regression)

#Run the rolling regression (Rolling window)

roll_expanding <- roll_regres(y ~ X1, df_1, width = 25L,do_downdates = FALSE)

#Check the last 10 coefficients

roll_expanding$coefs %>% tail(10)

## (Intercept) X1

## 191 1.189651 -1.066285

## 192 1.196722 -1.077508

## 193 1.180968 -1.068470

## 194 1.178508 -1.064603

## 195 1.177739 -1.064419

## 196 1.170369 -1.063868

## 197 1.172466 -1.064678

## 198 1.179917 -1.056945

## 199 1.181876 -1.056017

## 200 1.178556 -1.054890